IT’S EASY TO SAY IMPACT

By Paola Dubini

The focus on the sustainable development model proposed by the UN and the 17 goals of the 2030 Agenda is leading to an increasing diffusion in the international debate among institutions, academia and practitioners of three “strong” terms: sustainability, impact and accountability. They have long been prevalent among economists: the first2 has to do with the ability to endure over time, on the one hand adequately remunerating all factors of production, and on the other absorbing and indeed anticipating internal and external changes; the second concerns the spill over effects of economic activity on the economy of the company’s stakeholders, whether they are employees, suppliers or the territory in which the organization operates. Finally, the third term, evokes the idea of “accountability,” being responsible to third parties for given behaviours and given results3 . The three terms are strong because they are central not only in guiding the survival and growth of an organization, but also in the ways in which these are accomplished.

It is not a given that a company will last over time: changes in technology, regulation, or customer tastes, as well as longer-term social, economic, and institutional variations change the context for business operators. Different social, political and economic urgencies also significantly alter expectations of return and economic spillover; finally, the greater the articulation of an organization’s governance and the greater the sensitivity of public opinion, the more the meaning of reporting takes on a rich variety of nuances. From this point of view, the conceptual model underlying the 17 Sustainable Development Goals raises the bar in no small measure, because it broadens the scope of responsibility of each actor2 and the degree of interdependence between actors, increasing the number of areas in which each actor is evaluated3 . The conditions of efficiency (one of the factors of economic sustainability) must also cover the minimization of environmental impact on the one hand and the assessment of environmental risks on the operation of the organization on the other; adequate remuneration of factors of production includes making explicit the ways in which human rights are respected and equal opportunities guaranteed; and the reporting system is destined to incorporate more and more explicitly non-financial indicators, which will make it possible to appreciate -in addition to profitability and financial soundness- environmental sustainability and spill overs in the social sphere. In the case of European companies, the legislation is moving in the direction of making explicit a taxonomy of sustainable activities that companies can consider in reporting to document the ways in which they mitigate and offset their impact on the environment, and to be able to demonstrate that they are acting in a socially equitable and sustainable manner. The focus on sustainability indicators linked to non-financial elements1 is linked to the dual need to witness progress and to mitigate reputational risks associated with accusations of “washing”2 by an increasingly polarized public opinion amplified by social media.

Sustainability of cultural organizations

For cultural organizations, the sustainability conditions, the expectations of impact and the dimensions on which to “account” become more articulated. Their economic and patrimonial fragility is well known, while less well known is the prudence that characterizes their management and the ability of the most virtuous organizations to build conditions of economic durability; while it is true that -by virtue of their legal form- some cultural organizations “cannot fail”, it is equally true that the degrees of freedom in resource allocation choices and the alternatives available to achieve economic break-even are very limited. Depending on the areas of activity, reflecting on environmental sustainability opens up relevant issues of preservation (of buildings, collections, traditions) or presupposes significant changes in practices (think, for example, of large events, which are often energy-intensive and highly impactful because of the pressure on the mobility of the public and operators, on the production of waste, and on the infrastructure of the host territories). Incorporating issues of adaptation to climate change and mitigation of environmental effects can take on identity value for cultural organizations: the territory of Langhe Roero and Monferrato is a UNESCO heritage site to protect a landscape, a variety of villages and buildings, but also specific practices in the treatment of vineyards, production and preservation of specific wines. Climate change could challenge several elements of this heritage. Again, we are used to mega concerts at night: should we imagine that instances of energy conservation require having live shows during the day? And -in a country that has heritage protection as a constitutional responsibility- under what conditions is it reasonable to imagine placing photovoltaic systems on the roofs of historic buildings or wind turbines on the tops of mountains?

Regarding social impact, it is not difficult to recognize that cultural organizations perform a social function, because through activities of a cultural nature they contribute to the construction of citizenship, perform an educational and inclusive function. However, with few exceptions, cultural organizations struggle to come up with convincing arguments about the effectiveness and spill over effects of their actions; the transformative role of culture is recognized by those who practice it on an ongoing basis, while the rest of the community ignores or takes for granted their cultural function or measures it in terms of notoriety; the peer community recognizes the cultural role, but the community generally think about the impact generated using different categories.

Finally, with regard to accountability, the spread of social entrepreneurship projects has contributed to the growth of expectations of social returns from philanthropic investments1 that replicate resource allocation logics borrowed from the corporate world2 . This has prompted some organizations -particularly those with a social commitment- to account for the social impact generated. In the presence of dwindling public resources, the economic sustainability of cultural organizations increasingly relies on diversification of revenue sources and on governance mechanisms involving stakeholders of different natures (state, local authorities,businesses, individual donors); this makes it necessary to add to the typical reporting tools -which concern how public resources or those from institutional sources were spent- other documents that can highlight the quality of the work done and the benefits generated to the community as a whole by cultural activity.

Storytelling and measuring impact

The issue of impact generated by cultural organizations thus inevitably ties in with issues of economic governance and accountability. Impact is an “unwieldy” term because it presupposes forced contact and a significant effect, either immediately or over time, on a recipient. By their nature, cultural organizations generate impact over time, through a continuity of action: their size does not generally make immediate intensity of reaction possible. It is the ongoing effect of the gymnasium, not the disruptive effect of an uppercut, that produces a result. Even when the expected reaction is intense and immediate -as in the case of the demonstrations staged in major international cultural institutions by P.A.I.N. activists against the Sackler family, producers of a powerful opiate, or in the demonstrations by environmental activists exasperated by the community’s lack of initiative and sense of urgency- cultural organizations are often means and not active participants in generating impact, except over a medium-term time frame: empowered to contribute to the dannatio memoriae of the Sackler family, major museums have effectively refused further donations and removed the name of a very important donor from their halls and communication. Significant exhibitions of denunciation that have been talked about have often been contextualized, explained, told in an overall effort of mediation aimed at reaching wide slices of public opinion.

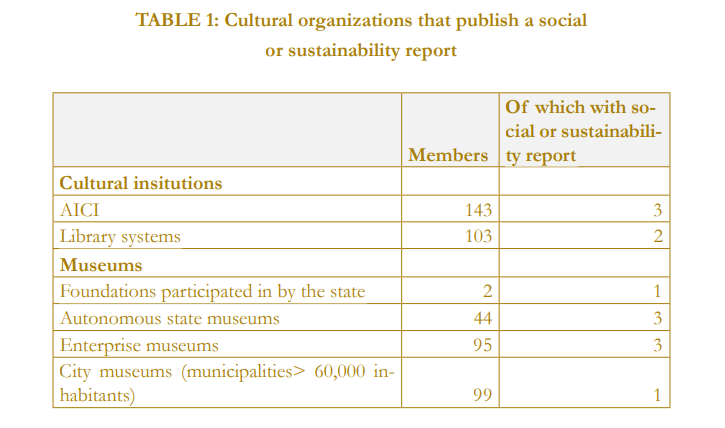

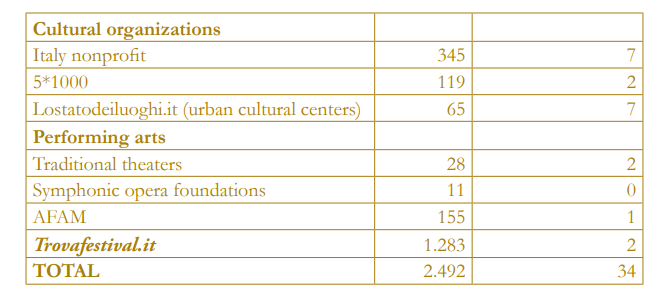

Moreover, like education, culture is a merit good1 : people do not necessarily feel the need for it; it is also an experiential good2 , whose value and importance cannot be assessed a priori; and finally it is a credence good1: even after it has been tried,it is difficult to assess its quality. And so it happens that those who would most benefit from the engaging, transformative or inclusive action of the arts do not feel the need for it or are unaware of its existence and potential. And even when they have been involved, awareness of the impact often occurs some time later. To understand in a systematic way how cultural organizations represent the impact they generate , we analysed how many organizations registered with specific associations, belonging to specific categories or mapped by different aggregators publish a social or sustainability report (Table 1). From this base, we collected through online keyword searches an additional 13 cases, totalling 47 organizations and 139 observations covering the years 2018-2021.

As can be seen, in the absence of legal requirements and in the presence of complex reporting systems, very few cultural organizations publish a social or sustainability report. Interestingly, however, the exercise is carried out proportionally more frequently by very small entities, suggesting that the sustainability report is a tool for communication and legitimacy with potential donors.

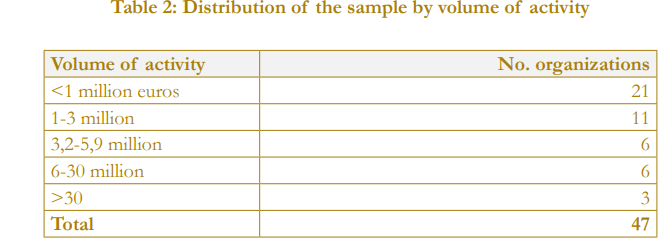

In their mission narrative, the organizations analysed emphasize cultural preservation and enhancement, promotion of artists, and the right to culture as tools of citizenship that is realized through educational, inclusion, and urban regeneration activities aimed at culturally based territorial development. Reference to Goals 4, 10, 11, and 16 of the 2030 Agenda is evident, although only 13 organizations in the sample explicitly refer to the Sustainable Development Goals in their financial report, particularly Goal 8 (10 cases) and Goal 11 (9 cases). Table 3 summarizes the impact areas made explicit in the financial reports considered. Data are expressed as percentages to account for the fact that several organizations cited more than one area; in evidence, the composition of the sample conditions the relative weight of the different impact areas. The most cited area of impact concerns the relationship with audiences: this is primarily translated into forms of community engagement with specific audiences (schools, families, ...), followed by the construction of non-formal learning opportunities through the languages of the arts and the digitization of collections, as well as the development of new audiences. The second most-cited area of impact relates to the activation of skills: the organizations in the sample create impact because they provide structured peer-topeer opportunities for those belonging to arts communities, because they enable a transfer of specialized skills, because they take action to create job opportunities for professionals in the arts, because they scout or anoint creative talents by pitching them to non specialist audiences.

The third direction of impact has to do with the enhancement of managed assets: from the growth of assets to the enhancement of facilities. Sometimes cultural organizations operate in spaces that lend themselves to different public uses; the provision of premises and green spaces is a possible direction of valorisation and stimulating the building of a sense of belonging. A further area of impact is related to research: the museums in the sample identify themselves as research institutions with a particular dissemination function. Producing exhibitions, materials on the one hand, hosting meetings for insiders, workshops and opportunities to relate different specialized knowledge for the benefit of broad audiences are ways through which they contribute to the production of new knowledge and stimulate curiosity.

The next area of impact is related to inclusion and social innovation: the mix of services offered, the availability of safe spaces, and the opportunity given to people to satisfy their curiosities and interests independently or through a guided offering are sometimes geared toward groups of people who are unfamiliar with cultural venues and who are excluded or self-excluded. The impact on the local area is linked to the ability to attract visitors, the activation of international networks and the collaborations put in place with local operators. Finally, in some cases management and cultural activities are oriented toward environmental sustainability and advocacy on environmental sustainability issues.

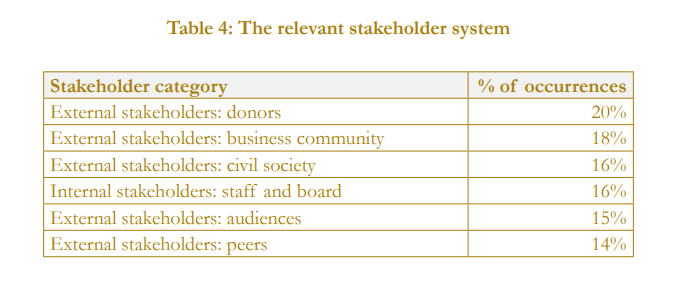

The quantitative indicators of the impacts generated refer in all cases to the number of people involved for different categories of audiences (total number, mix, effectiveness of online communication, etc.), the volumes of activities carried out (workshop days, number of exhibitions, articles published, collaborative projects activated, days and hours of opening, conferences...) and the resources used or mobilized (resources allocated, invested, collected). Moreover, depending on the strategy implemented, the quantitative indicators reported concern the characteristics of the processes (digitized collections, restoration campaigns, specific communication campaigns), audiences, the degree of loyalty and cultural participation activated, and the economic contribution generated for the territory. In addition, the financial statements generally present qualitative results resulting from specific surveys or observation activities, particularly of new audiences approached. The reference time horizons considered are either the year or longer time intervals. Progress achieved often focuses on specific themes (e.g., growth in the number of adolescents reached, evolution of revenue mix, change in audience retention rate). Indicators include efficiency metrics to testify to shrewd use of public resources (evolution in average time for setting up and taking down exhibitions, % of recycled materials used in setting up exhibitions). About a third of the surveyed organizations mention the professional collaborations activated and the mix of contracts in place. The focus on local communities has two sides: on the one hand, the number and duration of supply relationships at the local level, and on the other hand, the number of free initiatives offered, such as training opportunities offered for volunteers, professionals in cultural sectors, and young artists. If we analyse together the size of organizations and the directions of work to achieve cultural and social impact, a theme of critical mass becomes apparent. One of the relevant and specific aspects of sustainability reporting by cultural organizations is the explication of the depth, variety, quality and durability of the stakeholder networks to which cultural organizations are a part, which they help to create and against which they feel accountable. Table 4 summarizes the stakeholder categories mentioned.

All the organisations considered highlight different categories of stakeholders as their main interlocutors. Donors are the most frequently mentioned category (and include institutions, sponsors and patrons), with a particular focus on institutions (national and local). The business community includes suppliers, the media, economic operators in the area, including tourism operators. Civil society is declined into three specific categories: schools, residents, territorial associations. Some cultural organisations identify internal stakeholders as their main interlocutors: not only employees, but also board members. Finally, the possibility to create impact is linked to the articulation and quality of collaborations between peers, at national and international level: the most cited stakeholders in this category are universities, other cultural institutions, and natural attractions.

Concluding remarks

The dissemination of sustainability and social reports among cultural organisations is still very limited, and it is well known that reporting tools offer a partial view of the organisations’ strategy; however, the absence of obligations to publish social and sustainability reports and the relative freedom of narrative in this regard allow us to witness the transparency efforts of organisations that we often take for granted and hardly recognise in their cultural and social function. The analysis shed light on the different roles played by cultural organisations, the relationship between cultural and social impact, the areas of impact identified and their operationalisation. Furthermore, making explicit the system of stakeholders to whom the organisation feels accountable is a relevant step for organisations that are pervasive and taken for granted by their nature. Undoubtedly, much remains to be done to find timely indicators to help organisations account for (and then report on) the mark they make. However, research shows that the work of identifying the target audiences and impact dimensions sought presupposes a reporting logic and governance of organisations capable of embracing the breadth of challenges.

Paola Dubini is professor of management at Bocconi University in Milan, researcher at the ASK centre of the same university and visiting professor at IMT in Lucca. For about 20 years, her research and professional interests have been focused on the sustainability conditions of private, public and non-profit cultural organisations and on territorial policies for culture in a sustainable development perspective. She participates in the Boards and Technical Scientific Committees of several organisations active in the cultural and creative sectors and is the author of numerous publications. Among the most recent are: Dubini et al, “Institutionalising fragility”, Fondazione Feltrinelli (2016); Dubini et al, “Management of cultural organisations”, Egea (2017); Dubini, “Con la cultura non si mangia.falso!”, Laterza (2018).